In our latest post, we explained how to use ML + XAI to build strong generalized linear models with R. Let’s do the same with Python.

Insurance pricing data

We will use again a synthetic dataset with 1 Mio insurance policies, with reference:

Mayer, M., Meier, D. and Wuthrich, M.V. (2023),

SHAP for Actuaries: Explain any Model.

https://doi.org/10.2139/ssrn.4389797

Let’s start by loading and describing the data:

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

import seaborn as sns

import shap

from sklearn.datasets import fetch_openml

from sklearn.inspection import PartialDependenceDisplay

from sklearn.metrics import mean_poisson_deviance

from sklearn.dummy import DummyRegressor

from lightgbm import LGBMRegressor

# We need preview version of glum that adds formulaic API

# !pip install git+https://github.com/Quantco/glum@glum-v3#egg=glum

from glum import GeneralizedLinearRegressor

# Load data

df = fetch_openml(data_id=45106, parser="pandas").frame

df.head()

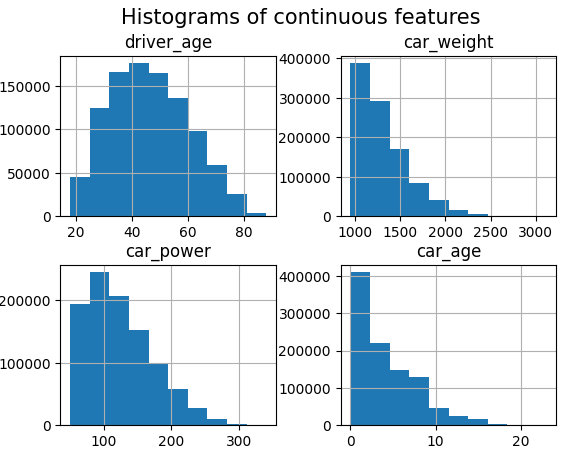

# Continuous features

df.hist(["driver_age", "car_weight", "car_power", "car_age"])

_ = plt.suptitle("Histograms of continuous features", fontsize=15)

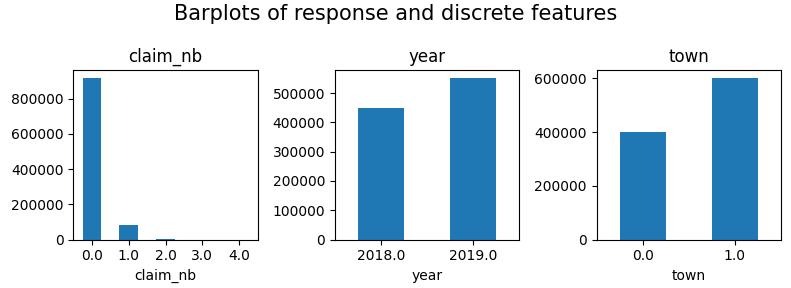

# Response and discrete features

fig, axes = plt.subplots(figsize=(8, 3), ncols=3)

for v, ax in zip(["claim_nb", "year", "town"], axes):

df[v].value_counts(sort=False).sort_index().plot(kind="bar", ax=ax, rot=0, title=v)

plt.suptitle("Barplots of response and discrete features", fontsize=15)

plt.tight_layout()

plt.show()

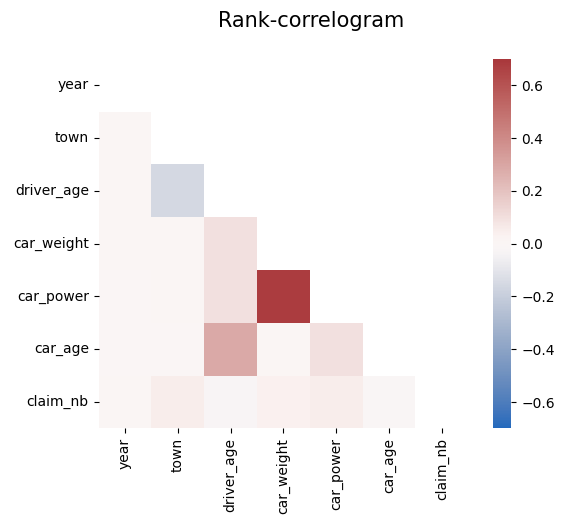

# Rank correlations

corr = df.corr("spearman")

mask = np.triu(np.ones_like(corr, dtype=bool))

plt.suptitle("Rank-correlogram", fontsize=15)

_ = sns.heatmap(

corr, mask=mask, vmin=-0.7, vmax=0.7, center=0, cmap="vlag", square=True

)

Modeling

- We fit a tuned Boosted Trees model to model log(E(claim count)) via Poisson deviance loss.

- And perform a SHAP analysis to derive insights.

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(

df.drop("claim_nb", axis=1), df["claim_nb"], test_size=0.1, random_state=30

)

# Tuning step not shown. Number of boosting rounds found via early stopping on CV performance

params = dict(

learning_rate=0.05,

objective="poisson",

num_leaves=7,

min_child_samples=50,

min_child_weight=0.001,

colsample_bynode=0.8,

subsample=0.8,

reg_alpha=3,

reg_lambda=5,

verbose=-1,

)

model_lgb = LGBMRegressor(n_estimators=360, **params)

model_lgb.fit(X_train, y_train)

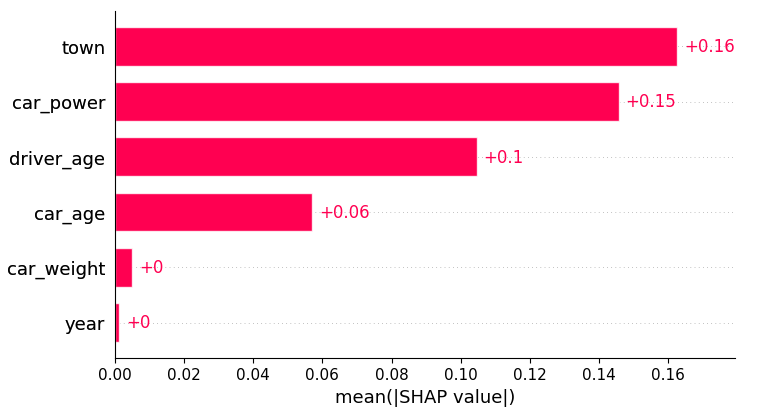

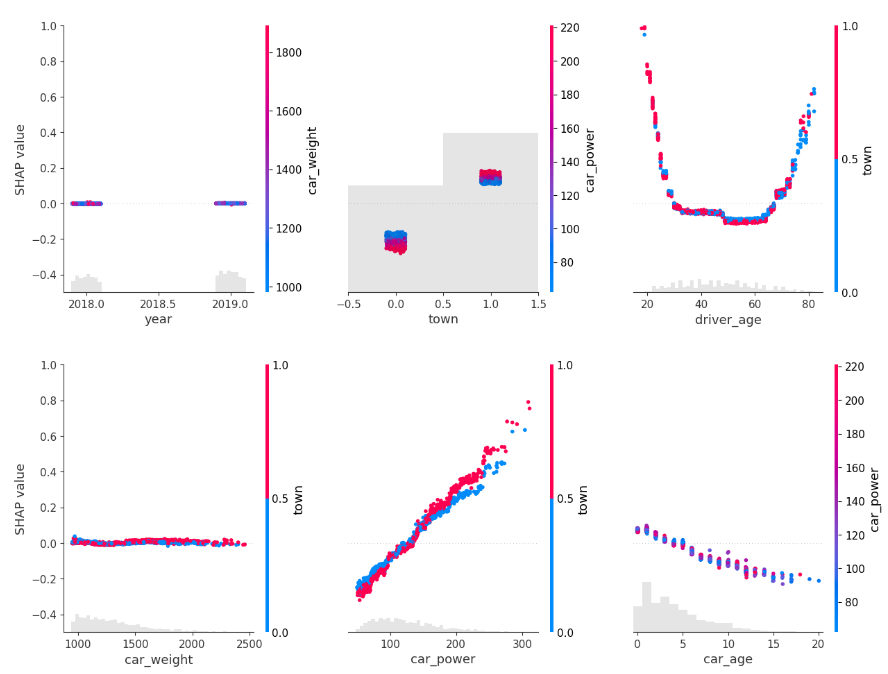

# SHAP analysis

X_explain = X_train.sample(n=2000, random_state=937)

explainer = shap.Explainer(model_lgb)

shap_val = explainer(X_explain)

plt.suptitle("SHAP importance", fontsize=15)

shap.plots.bar(shap_val)

for s in [shap_val[:, 0:3], shap_val[:, 3:]]:

shap.plots.scatter(s, color=shap_val, ymin=-0.5, ymax=1)

Here, we would come to the conclusions:

car_weightandyearmight be dropped, depending on the specify aim of the model.- Add a regression spline for

driver_age. - Add an interaction between

car_powerandtown.

Build strong GLM

Let’s build a GLM with these insights. Two important things:

- Glum is an extremely powerful GLM implementation that was inspired by a pull request of our Christian Lorentzen.

- In the upcoming version 3.0, it adds a formula API based of formulaic, a very performant formula parser. This gives a very easy way to add interaction effects, regression splines, dummy encodings etc.

model_glm = GeneralizedLinearRegressor(

family="poisson",

l1_ratio=1.0,

alpha=1e-10,

formula="car_power * C(town) + bs(driver_age, 7) + car_age",

)

model_glm.fit(X_train, y=y_train) # 1 second on old laptop

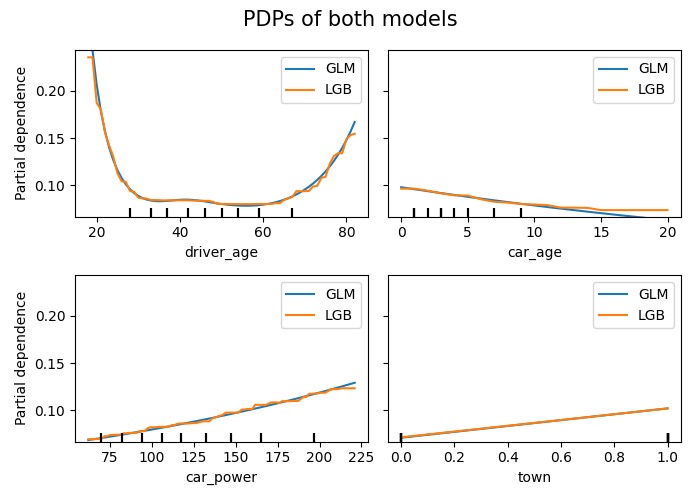

# PDPs of both models

fig, ax = plt.subplots(2, 2, figsize=(7, 5))

cols = ("tab:blue", "tab:orange")

for color, name, model in zip(cols, ("GLM", "LGB"), (model_glm, model_lgb)):

disp = PartialDependenceDisplay.from_estimator(

model,

features=["driver_age", "car_age", "car_power", "town"],

X=X_explain,

ax=ax if name == "GLM" else disp.axes_,

line_kw={"label": name, "color": color},

)

fig.suptitle("PDPs of both models", fontsize=15)

fig.tight_layout()

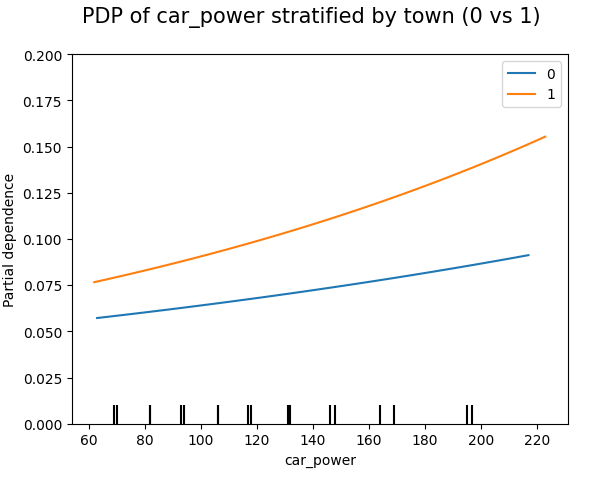

# Stratified PDP of car_power

for color, town in zip(("tab:blue", "tab:orange"), (0, 1)):

mask = X_explain.town == town

disp = PartialDependenceDisplay.from_estimator(

model_glm,

features=["car_power"],

X=X_explain[mask],

ax=None if town == 0 else disp.axes_,

line_kw={"label": town, "color": color},

)

plt.suptitle("PDP of car_power stratified by town (0 vs 1)", fontsize=15)

_ = plt.ylim(0, 0.2)

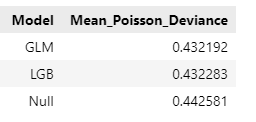

In this relatively simple situation, the mean Poisson deviance of our models are very simlar now:

model_dummy = DummyRegressor().fit(X_train, y=y_train)

deviance_null = mean_poisson_deviance(y_test, model_dummy.predict(X_test))

dev_imp = []

for name, model in zip(("GLM", "LGB", "Null"), (model_glm, model_lgb, model_dummy)):

dev_imp.append((name, mean_poisson_deviance(y_test, model.predict(X_test))))

pd.DataFrame(dev_imp, columns=["Model", "Mean_Poisson_Deviance"])

Final words

- Glum is an extremely powerful GLM implementation – we have only scratched its surface. You can expect more blogposts on Glum…

- Having a formula interface is especially useful for adding interactions. Fingers crossed that the upcoming version 3.0 will soon be released.

- Building GLMs via ML + XAI is so smooth, especially when you work with large data. For small data, you need to be careful to not add hidden overfitting to the model.

Leave a Reply